The Senior Preferred has been paid back. When will Treasury admit it?

Will the Trump administration actually reverse the Net Worth Sweep and admit Fannie Mae ($FNMA) and Freddie Mac ($FMCC) have repaid their bailout obligations?

This is my second recent article on GSE capital reform. Part of my long-term buy-side coverage of Fannie Mae ($FNMA) and Freddie Mac ($FMCC). My prior article walked through the ERCF revision thesis and stipulated that regulatory dominoes have been set off by Trump’s March 2026 executive order and the Fed’s banking capital proposals. This article focuses on the $373 billion guerilla in the room: Treasury’s Senior Preferred Stock (SPS). I believe it will get resolved in a manner that is favorable to shareholders. But there are significant risks (as many JPS holders have correctly pointed out over the years) and investors should be clear-eyed about this.

A quick recap

The SPS is one of the most contentious and confusing aspects of the investment case for Fannie Mae and Freddie Mac.

In September 2008, Treasury put Fannie and Freddie into conservatorship and signed the Preferred Stock Purchase Agreements. In return for an unlimited backstop, it received non-voting senior preferred stock in each GSE plus warrants to buy 79.9% of the common at a nominal price, expiring September 7, 2028.

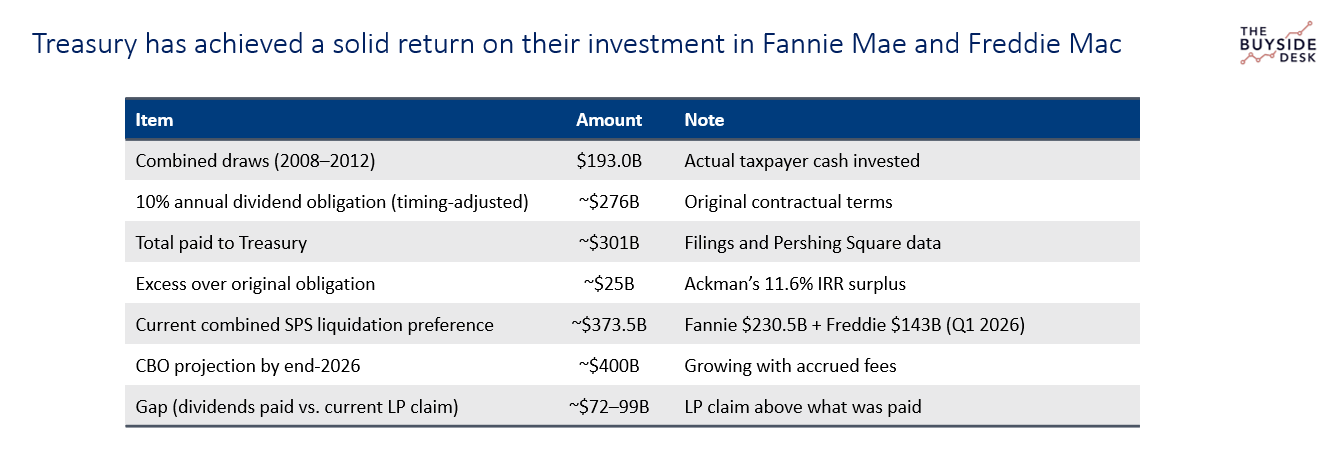

The GSEs drew a combined $193 billion between 2008 and 2012. That amount was added straight to the liquidation preference. Treasury was owed 10% annual dividends on the outstanding balance (12% if missed). The GSE’s were forced to mark losses to market via (unfair and unrealistic) loss provisions. Under that strain, they could not reliably pay dividends on the SPS amount. But the losses never materialized, and just as the companies were about to reverse the accounting provisions, and thereby repay Treasury in full (with interest), the government unilaterally amended the PSPA to sweep of every dollar of net worth above a tiny reserve. That’s the Net Worth Sweep.

Under this shameful agreement, Fannie and Freddie have sent Treasury roughly $301 billion. Yet the SPS liquidation preference never shrank. Instead if grew. As of Q1 2026, Fannie’s stands at $230.5 billion, Freddie’s at $143 billion. Combined: $373.5 billion. The CBO sees it climbing toward $400 billion by year-end as commitment fees keep accruing.

The paradox is obvious. They paid back more than they borrowed, with interest, but Treasury’s contractual claim is larger today than when the checks first went out.

**Note: I know this has glossed over many details on the Net Worth Sweep. But it will have to suffice for the purposes of this article.

The Money Arithmetic

Bill Ackman and Pershing Square laid this out in November 2025. The numbers hold up better than the critics admit.

Under the original PSPA, Treasury was entitled to 10% dividends on the outstanding liquidation preference. Run the actual $193 billion draws through a timing-adjusted 10% calculation and you get roughly $276 billion in total contractual dividends owed. The GSEs have paid $301 billion—about $25 billion more than the deal required. That works out to an internal rate of return for Treasury of roughly 11.6%.

Ackman’s core point: the economic substance of the investment has been satisfied. The government took real risk when it mattered most and collected more than the agreed return. The $373.5 billion liquidation preference is a legal artifact of how preferred equity works in that dividends don’t reduce principal, and the LP was designed to grow, not shrink. The Net Worth Sweep itself is Exhibit A: without the 2012 amendment, normal dividend mechanics might have allowed a repayment path; instead, the sweep extracted every available dollar.

By any normal investment metric, Treasury got its money back plus a solid return. But the instrument is preferred equity, not a loan. The contract doesn’t contain a repayment mechanism that reduces the LP when dividends are paid. Unfortunately for shareholders, both realities can coexist: taxpayers were made more than whole on an economic basis, and Treasury still holds a $373.5 billion contractual claim. This has been upheld by the courts despite considerable efforts to fight it. Resolving this claim is a political and administrative call. Neither Congress or the courts will help.

The Five Possible Paths to Resolution

There’s no single button. Here are the five plausible structures, each with different effects on the capital stack, the budget, investors, and the mortgage market.

Administrative PSPA amendment (Ackman-style “deemed repaid”): Treasury and FHFA amend the agreements to declare the SPS economically satisfied and zero out (or nominalize) the entire liquidation preference. No new legislation needed. Then exercise the warrants for 79.9% of the common on a fully diluted basis. Treasury ends up owning exactly 79.9% of the common equity; existing common holders retain 20.1%. Cleanest path for relisting.

Full LP-to-equity conversion: Amend the PSPA to convert the entire $373.5 billion LP directly into new common shares at a negotiated price per share. Combined with warrant exercise, this would push Treasury’s ownership well above 80%—likely 90–95%+ depending on the conversion ratio and enterprise value. Massive dilution for everyone else.

LP-to-debt conversion: Turn the SPS claim into long-dated GSE bonds. Moves it out of the equity stack and helps with ERCF capital treatment, but adds leverage and doesn’t fully clean the structure.

Guarantee fee / explicit backstop: Cancel the SPS in exchange for an ongoing annual guarantee fee on agency MBS. Mirrors the Ginnie Mae model—explicit, priced government backing.

Hybrid (partial forgiveness/restructuring + warrant exercise + residual SPS): Forgive or restructure a portion of the LP (say, the economic “excess” plus some negotiated amount), exercise the warrants for the 79.9% stake, and leave a reduced residual SPS on the books (perhaps $150–250 billion after partial write-down/conversion). Treasury secures dominant but not total ownership.

Paths 1-3 and 5 are feasible without Congress, though PAYGO budget scoring is a practical hurdle. The guarantee-fee route almost certainly needs legislation. The Hybrid path depends heavily on the terms “negotiated” (in quotation marks since the government will negotiate with itself on this one).

A quick note on how the Hybrid and Deemed Repaid Paths Compare

Importantly, the Trump administration’s “North Star” in this process are (1) reducing mortgage rates (or at least not making changes that increase them) and (2) achieving an IPO of Fannie and Freddie. As such, the “Pure Repaid” vs. “Hybrid” path decision matters greatly.

Pure Deemed Repaid (Ackman proposal): The entire $373.5 billion LP is extinguished to zero or nominal. No residual senior claim remains. The Net Worth Sweep ends completely. Treasury exercises the warrants and owns exactly 79.9% of the common; existing common keeps 20.1%. The balance sheet is clean—no ongoing dividend priority ahead of private shareholders. This maximizes enterprise value (higher trading multiples because public investors see a true privatization story), supports faster capital deployment, and makes a successful NYSE relisting far easier. It also aligns cleanly with lower mortgage rates: no overhang means the GSEs can operate with stronger perceived stability, potentially allowing g-fee relief without spooking MBS markets. Key Downside: larger upfront budget scoring hit.

Hybrid Path: A chunk of the LP (roughly $100–150 billion, starting with the IRR excess) gets forgiven or restructured. Another slice may convert to debt or equity. But a meaningful residual SPS stays on the books at a reduced level, still senior to both junior preferreds and common, with a modified dividend or accrual obligation (e.g., 10% or lower on the smaller balance). Treasury still exercises the warrants for its 79.9% common stake; existing common keeps the same 20.1% post-dilution. The companies must continue servicing that residual SPS first, which forces heavier earnings retention on top of ERCF requirements. Result: delayed or minimal dividends to junior preferred and common for years, a valuation drag (public investors discount the stock for the lingering senior claim), and slightly messier IPO optics. It does offer better political cover and a smaller budget score, but it complicates the IPO goal and could subtly weigh on MBS pricing if markets see incomplete resolution.

In short, the deemed-repaid path delivers the cleanest capital structure for a high-quality IPO and the strongest support for lower housing costs. The hybrid trades some of that cleanliness for easier politics and scoring. The major question would be how much does President Trump care about politics and budget scoring?

The Ackman Path: Administrative Amendment

In my opinion, this remains the cleanest, fastest option. Amend the PSPA (the sixth time) to acknowledge the SPS as satisfied, zero the LP, exercise the warrants, and relist. Treasury walks away with 79.9% of the common in two much stronger companies.

Why taxpayers should like “deemed repaid”: instead of clinging to an illiquid $373 billion LP claim of uncertain collectability, Treasury gets roughly 80% of a relisted, growing enterprise that analysts peg at $300–400 billion combined enterprise value (potentially higher once the overhang is gone and ERCF revisions take hold). That equity stake could easily be worth $240–320 billion in market value, with upside from future sales or dividends. Full conversion to 100% ownership would essentially nationalize the firms, crush private-market discipline, tank valuation multiples, invite more litigation, and look politically radioactive. Eighty percent is already ironclad control without those downsides. The warrant expires September 7, 2028. Technically Treasury could unilaterally change the deadline, but why should they when a clearer and simpler path is in front of them.

Other paths that require Congress to act are non-starters. Congress has not acted on this issue for going on 18 years and is unlikely to start now.

My thesis: the SPS gets resolved via the “deemed repaid” path because this is how Treasury can best satisfy their own stated priorities: lowering mortgage rates and housing finance costs while delivering a credible IPO and conservatorship exit.

The IRR math is real and publicly defensible. The Net Worth Sweep extracted more cash than the original terms contemplated. The warrant clock is ticking. The ERCF revision running in parallel removes the old capital-gap excuse. And this Trump administration is the most privatization-minded since the conservatorship began.

…But there are significant, and very real, challenges

There are legitimate challenges to the “deemed repaid” path that investors should be aware of.

First, the SPS was never structured as a loan. It’s preferred equity. Dividends don’t reduce principal by design. Legally, Treasury can’t just declare it “repaid” without an amendment that survives scrutiny [Note: they are negotiating with themselves, so they it has to survive their own scrutiny…if that makes any sense]

Second, budget scoring would sting. CBO/OMB might treat extinguishing $373 billion as a large one-time cost, triggering PAYGO issues. However, it is unclear how much the Trump administration would prioritize this consideration. [Note: the appointment of Marc Calabria to OMB, where he serves as Associate Director for Treasury, Housing and Commerce will almost certainly make this an issue]

Third, litigation risks from JPS holders. Cancelling the LP (SPS deemed repaid) moves them up the capital stack and materially improves their odds of par recovery as well as dividend reactivation. But they could still sue if Treasury’s PSPA amendment to deem SPS repaid funnels value straight to Treasury’s warrants/commons without explicit priority for JPS.

Fourth, optics about “bailing out hedge funds” is real. But I suspect the Trump administration does not have this very high on their priority list.

What to watch for in the coming months

FHFA’s July 2026 report: concrete language on SPS treatment under capital reform is a strong signal

Public comments from Secretary Bessent or Director Pulte on the IRR math, “taxpayers made whole,” or IPO timing

Any OMB/Treasury signals on budget scoring for PSPA changes

Warrant-exercise authorization

Litigation settlements or congressional noise on explicit guarantees

I have long advocated for the SPS being deemed repaid…

To me, the “SPS deemed repaid” thesis is the most compelling and contested idea in the GSE trade. The economics are real, the administrative tools exist, the clock is ticking, and the administration’s own priorities of lower mortgage rates and a successful IPO/end to conservatorship now point strongly toward the cleanest resolution possible.

I expect a structured sixth PSPA amendment that extinguishes the vast majority (or all) of the LP, exercises the warrants for Treasury’s 79.9% common stake, and sets up a clean transition out of full conservatorship. Any hybrid elements would be engineered with a minimal or rapidly vanishing residual SPS to avoid undermining the IPO or rate goals. To the extent that the “explicit-guarantee” approach is tried, it will be handed to Congress to run in parallel. More likely, it gets quietly dropped.

By deeming SPS repaid and extinguishing the LP, Treasury gets a story it can defend, materially improves JPS recovery odds (cleaner waterfall, closed capital gap), dilutes common via the warrant (as always expected), leaves MBS and senior debt largely untouched, and hands taxpayers 80% of two growing companies rather than a stale LP claim.

…but the trade remains binary on the PSPA terms

Watch for language on an ERCF revision. This is likely to be the first major signal that Fannie and Freddie will exit conservatorship before the end of President Trump’s term.