Huge changes are coming for Fannie Mae & Freddie Mac

The ERCF is about to change, and if the SPS is deemed repaid then both GSEs are ready to exit conservatorship almost immediately

Both Fannie and Freddie reported Q1 2026 earnings recently. As usual, headline numbers were astonishing for companies trading over-the-counter. Fannie earned $3.7 billion, Freddie $3.6 billion. Both beat expectations (as usual) and their combined net worth hit $186.6 billion. But investors have been accustomed to strong results for years now. This article is about what is happening behind the scenes. I think a tectonic shift is about to occur and it will put the GSEs on a pathway to exit conservatorship.

Over the last few quarterly updates, a curious re-framing of capital levels has not gone unnoticed. For instance, see the quote below from Freddie Mac CFO Jim Whitlinger’s prepared remarks

"Excluding buffers, our capital shortfall was $105 billion at the end of the first quarter, largely because the $73 billion of Senior Preferred Stock does not qualify as regulatory capital."

Read that again. He is saying that, as a technical matter, if its $73 billion of Senior Preferred Stock (SPS) qualified as regulatory capital their capital shortfall (excluding buffers) would collapse from $105 billion to roughly $32 billion. And that is against the current, unreformed ERCF. Pair that with a revised ERCF and the math shifts dramatically. [Note: Treasury’s SPS does not meet the ERCF’s Basel III-aligned capital definition, and we will return to this later]

In my previous article A golden window of opportunity for Fannie Mae and Freddie Mac I outlined why the Fed’s recent capital rule changes for MBS represented a big opportunity for FHFA to revise the ERCF. It makes no sense for the GSEs to have capital requirements more punitive than banks for the same underlying asset class. A simple harmonization of ERCF to make it consistent with the new regime is a clearly logical step.

Since this article, there have been some new developments. Largely, and surprisingly, unnoticed by most investors in Fannie Mae and Freddie Mac. Three things are now in motion simultaneously: Trump’s March 2026 executive order directed FHFA to revise capital requirements. The Fed/OCC/FDIC published 1,500 pages of proposed banking capital reforms on March 19. And the SPS acting as a giant pain in the capital stack. This last point is increasingly being framed by both the companies themselves as an obstacle to be dissolved, not managed around. These positions, taken by executives at both GSEs, would have been unthinkable under previous administrations (including Trump’s first term).

If all three resolve, both GSEs could technically exit conservatorship the day the ERCF final rule takes effect. No waiting. No IPO required to fill a capital hole. The timeline moves becomes very feasible within President Trump’s current term.

The Regulatory Chain Reaction begins…

1. The Executive Order

On March 13, 2026, Trump signed ‘Promoting Access to Mortgage Credit,’ a housing affordability-focused EO that, for our purposes, does two specific things. It tells the Fed, FDIC, OCC, and NCUA to revise capital regulations for banks which includes risk weights on portfolio mortgages, mortgage servicing rights, and warehouse lines. And it tells FHFA to consider revising capital requirements and to submit a report within 120 days recommending changes.

The 120-day clock expires mid-July 2026. That report is the first hard milestone in the ERCF revision story, and the market will parse every word of it.

The underlying logic is straightforward: GSE guarantee fee pricing is a direct function of capital requirements. When the Biden administration implemented the ERCF in its g-fee pricing in 2022, average fees jumped 7–10 basis points overnight — from the 45-48 bps range to roughly 55 bps. The GSE share of new mortgage originations has declined every year since, hitting 37.6% in 2025, the lowest in nearly two decades. The administration’s position is that this outcome is incompatible with its stated goal of making mortgages affordable. The EO is the opening bid on reversing it.

2. The Banking Capital Overhaul

On March 19, only six days after the EO, the Fed, OCC, and FDIC jointly released the most significant recalibration of U.S. bank capital requirements since the post-crisis reforms. Three separate NPRMs, spanning 1,500 pages, with comments due June 18. The relevant provisions:

— LTV-based tiering for residential mortgage risk weights, replacing the flat 50% standard weight. Lower-LTV loans get meaningfully lower charges.

— The securitization risk weight floor drops from 20% to 15%, reducing capital charges on agency MBS holdings at banks.

— Mortgage servicing asset capital deductions are replaced with a flat 250% risk weight — a net improvement for most community banks.

— Overall bank capital requirements decrease modestly across the board, with larger cuts for smaller, more traditional lending-focused institutions.

The direction is unambiguous. The agencies are explicitly trying to ease credit conditions in the mortgage market. And here’s the problem that creates for the ERCF: the ERCF was designed to mirror the ‘advanced approaches’ framework used by the largest U.S. banks. If the banking framework those requirements were anchored to is now being revised downward, maintaining an ERCF calibrated to the old, more conservative version is analytically incoherent.The GSEs would be required to hold capital against the same credit risks at a higher rate than the banks who buy their paper. That cannot stand, and the EO signals that Washington knows it.

Independent analysis at the time the ERCF was adopted estimated that actual capital needed for safety and soundness, based on Fannie’s and Freddie’s own stress test results, was $120-135 billion combined. The ERCF demanded $312 billion, or a whopping 2.4x what the stress tests indicated. Since then, both companies’ stress test results have improved materially.

3. The Capital Math

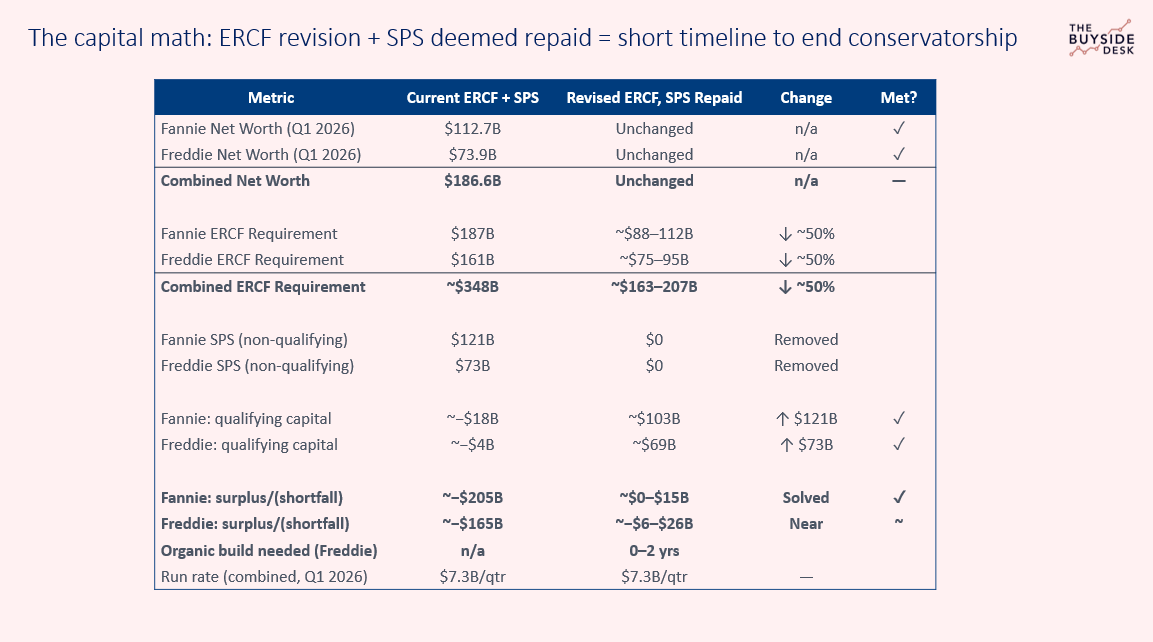

Now, using yesterday’s actual Q1 2026 numbers, here’s what the capital picture looks like across four dimensions: current ERCF requirements, the SPS deduction, the effect of a revised ERCF, and where each enterprise lands if you combine both.

Lets walk through the figures in the above table. Fannie Mae’s adjusted total regulatory capital deficit was approximately -$18 billion at Q1 2026 (vs. total requirement, including buffers, of around $205 billion). That looks daunting. But that -$18B figure is almost entirely the result of one thing: the $120.8 billion of SPS on Fannie’s balance sheet is subtracted from regulatory capital because Treasury’s preferred doesn’t meet the ERCF’s qualifying capital definition.

Treasury deeming the SPS repaid changes picture dramatically. Fannie’s ERCF-qualifying capital jumps to approximately $103 billion. Against a revised ERCF requirement in the $88–112 billion range, Fannie is at or near compliance right now. Not in five years. Right now.

Freddie’s picture is almost identical in structure, if somewhat tighter in the numbers. As CFO Whitlinger stated on yesterday’s call, the $73 billion SPS is “largely” responsible for the $105 billion capital shortfall (excluding buffers). Remove that deduction, and Freddie’s qualifying capital becomes approximately $69 billion. Against a revised ERCF minimum (excluding buffers) in the $47–60 billion range, Freddie meets minimum requirements immediately. It would still need to build into full buffer compliance of roughly $6–26 billion depending on the revised calibration. At a current run-rate of $3.6 billion quarterly earnings, this puts Freddie Mac on pace to close the gap within 1–2 years.

The combined run rate is $7.3 billion per quarter — $29.2 billion annualized. Any remaining buffer gap after a revised ERCF + SPS resolution closes within a few quarters. Not years. Quarters.

A plausible timeline emerges…

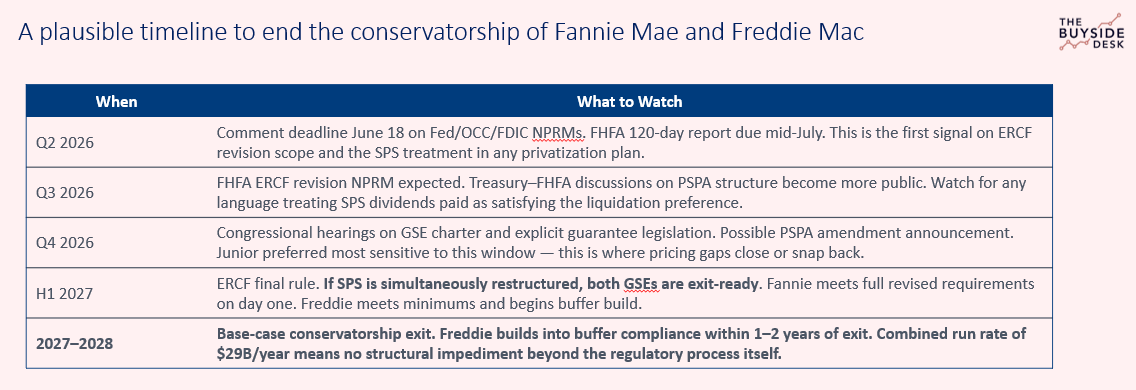

Revising the ERCF requires a formal APA notice-and-comment rulemaking that includes a proposed rule, comment period and a final rule. The July 2026 report is not the rule; it’s the preview. The most realistic sequencing from there: proposed rule in Q3 2026, comment period through late 2026, final rule in H1 2027. That timeline lands the ERCF final rule in the same window where PSPA resolution discussions will be at their most advanced. The two processes are running in parallel, not sequentially.

A note of caution: Treasury’s SPS decision is a wildcard

I have long advocated that the simplest and most logical solution for Treasury to deal with their SPS is to simply recognize past dividend payments and deem it repaid. But investors need to be clear eyed that this is uncertain. There have been no indications from Treasury as to their preferred course of action, and this remains the single biggest risk to the timeline above and to shareholders in the companies.

I will do a follow-up article going into the details of what Treasury could do with their SPS in a subsequent article. Suffice to say, if you believe that the SPS being deemed repaid is a likely path, then the recent Executive Order and Fed Capital Rule changes mark a significant milestone. One way or another, investors won’t need to wait long - Q2 2026 could herald a major signal for whether Fannie Mae and Freddie Mac exit conservatorship during President Trump’s current term.