Why Applied Materials shares are ready for lift-off

After taking a 40% hit over the last 7 months, a significant rebound could be in the works. I think the stock could double from today's levels.

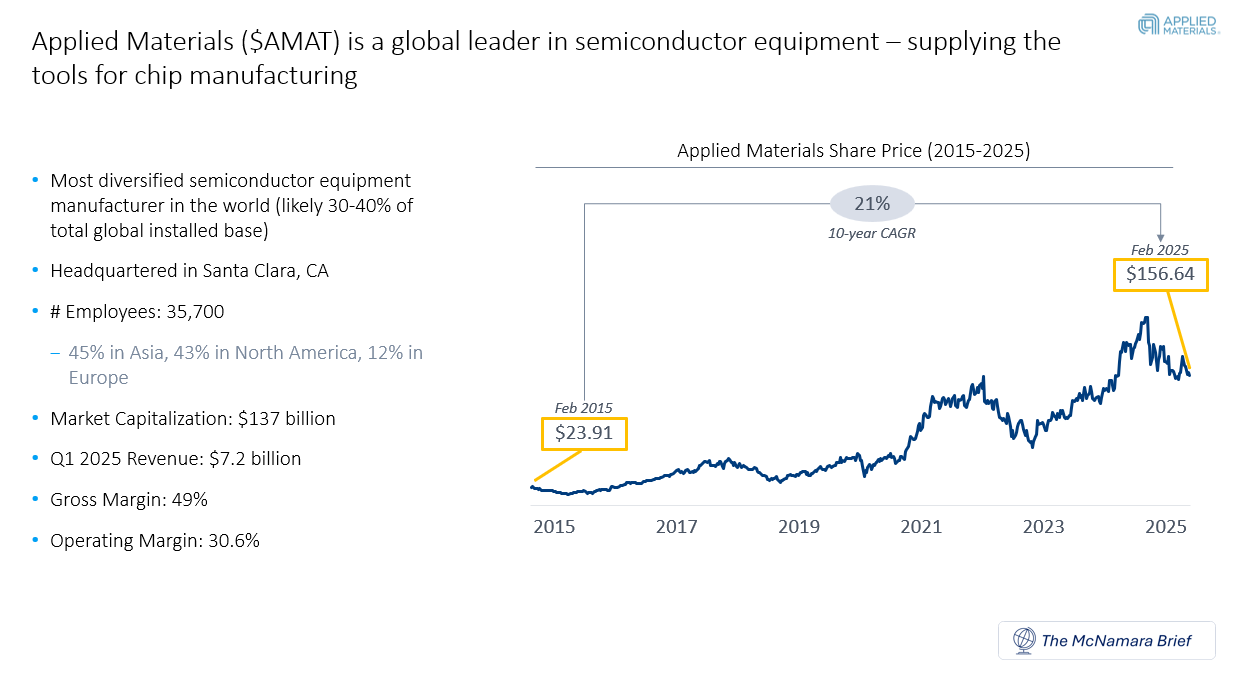

Greetings from The McNamara Brief! Today I’m sharing my investment case for Applied Materials (AMAT), a global leader in semiconductor manufacturing equipment. Over the last 7 months, this stock has been pummeled, down 40% drop from its highs. However, the business is stronger than ever and I believe AMAT offers a compelling opportunity for value investors.

Applied Materials is a global leader in semiconductor equipment. In other words, they make the tools that make semiconductors. When you hear about companies like NVIDIA in the news, they contract out the manufacturing of their semiconductors to “contract manufacturers”. These companies use the tools supplied by Applied Materials to make the chips. This is a highly technical and complex engineering process, requiring AMAT to be embedded with chip manufacturers at each phase of the manufacturing process.

In other words, AMAT is very hard to replace and they are very good at what they do. By some estimates, they have ~40% of the total global installed base for semiconductor production equipment (that comes with a very lucrative services business as well). Some quick figures:

Q1 2025 revenue: $7.2 billion

Gross Margins: 49%

Operating Margins: 30.6%

Let that sink in for a moment. Here we have a US based B2B manufacturer of industrial tools – and they have operating margins over 30%. Clearly, they have pricing power and a technological edge that acts as a serious barrier to entry in their markets. Over the past decade, its stock has compounded at 21% annually, despite the recent pullback. Those are some serious returns.

And the company has never been as financially strong as today.