TikTok Takedown: National Security and a huge M&A deal in the making?

TikTok is set to "go dark" on Jan. 19 2025. TikTok's story has ramifications for other social media platforms - and potentially for investors who can get in on the action

In August 2018, ByteDance (a Chinese company) launched a new social media application in the United States. It focused primarily on user generated short-form videos. It was something new. Something fresh. And it took the country by storm – especially among younger demographics. Competing platforms were stunned by the rise of this new competitor. In the years to follow, virtually all of them introduced features to emulate the short-form video craze. But it seemed there was just no stopping this new company. TikTok had become a phenomenon.

By 2024, TikTok had over 120 million users in the United States. Over 70% are under the age of 34 (about half of which were under 25) – a key demographic for advertisers. On average, American users spent just under 2 hours a day on the platform [a figure your author finds mind-boggling]. All of this was driven TikTok’s proprietary video recommendation algorithm which seemed to have cracked the code to getting, and keeping, user’s attention.

But suddenly it all seemed to turn. The US government stepped in with concerns over national security – and they weren’t messing around. They demanded TikTok be sold, as a stand-alone American company, to American owners or be banned. The company sued, saying this violated the First Amendment protecting their free speech. They lost. Badly. On January 19th, 2025 – 4 days from the date of this writing – TikTok, one of the most popular communications platforms in the United States, is poised to “go dark”.

But why exactly? How did this come about? And critically – is there any money to be made? Answering these questions is more difficult than it seems. There are devils in the details – and that makes it interesting. A TikTok divestiture could mean a company worth over $80 billion coming to market. For investors with access, this may be extremely lucrative. But before we get to that, we first must ask: what is TikTok anyway?

What is TikTok?

TikTok is a social media platform that allows users to create, upload and watch short video clips overlaid with text, voice overs and music. For each viewer, the platform creates a continuous sequence of videos based upon that user’s behavior, preference and other factors. TikTok’s goal: keep users engaged and on the platform. The platform captures attention, which they then sell to advertisers. In 2023, TikTok’s US advertising revenue was $16 billion – more than competing American platforms Snap and X combined.

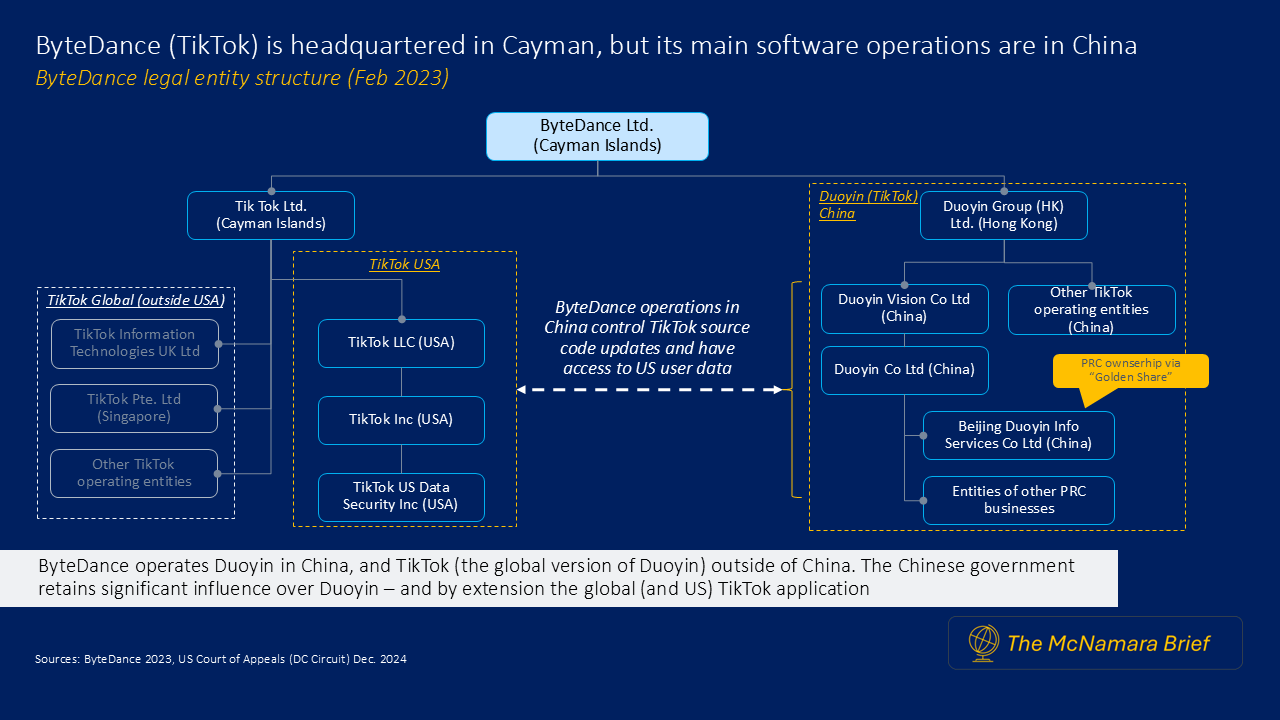

The “secret sauce” behind this incredible, and rapidly growing, business is TikTok’s recommendation engine. This is the algorithm that displays videos based on content metadata and user behavior. It identifies a pool of candidate videos for a user, then scores and ranks those videos using machine learning models. These models determine which video(s) would be most appealing to the user (to keep them engaged on the platform). Embedded in, the recommendation algorithm is TikTok’s content moderation process. Content moderation is achieved through video “heating” (i.e. video promotion) and “filtering” (video demotion). Decisions on which videos to heat or filter are internal company decisions. TikTok’s video “heating” decisions are taken by moderators in the local region or country. But video “filtering” decisions are taken at the central headquarters level and are heavily influenced (if not outright controlled) by ByteDance’s operations in China.

For the US government, and for the courts – this is a critical distinction, and a big problem.

China changes the rules for its companies

Key to this story is that legal changes don’t only happen in the United States. New laws are being written in every country – including China (where TikTok’s parent company ByteDance operates). Over the last decade, China passed two new “national security laws” and began forcing companies to integrate communist party cells into their management structures. Together, these developments caught the attention (and concern) of US regulators.

Technically speaking, requiring communist party committees to be embedded in Chinese companies was not new. This requirement has been in place since 1949 (when the country was founded). Back then, every company was state-owned so it made sense the ruling communist party would exert control. However, as decades passed and the economy grew, this requirement ceased to be enforced except for in the large state-owned enterprises. For those companies, the Chinese Communist Party retained key personnel decisions. However, the legal requirement remained in the books. In 2015, Chinese government policy shifted, and enforcement returned. Companies across China – including subsidiaries of foreign companies – were required to establish these committees. By 2021, the Chinese government reported that they had “achieved complete coverage” of the top 500 private companies in China. Further expansion to cover more companies is ongoing.

As enforcement of this old law was returning, China also passed The National Security Law of 2015. This law requires all citizens and corporations to provide support to national security authorities. Put simply, this required cooperation with any government request or investigation on any matter. If this wasn’t clear enough, in 2017 China passed a cybersecurity law that requires all companies to give the Chinese government full access to all their data and cooperate with any government investigation.

Under these circumstances, it is hard to believe anyone in China would dare not to comply with any government request on any matter at any time. For the US government, it means that even “private” companies in China are unable to act independently of the government. US officials called it China’s “hybrid commercial strategy”.

America responds to China’s legal changes

As things changed in China, so to did things in the United States. Suspicions rose that the Chinese government had too much influence over their companies operating in the United States. This was especially true of “Information and Communications Technology and Services” (ICTS) companies – i.e. social media platforms.

In May 2019, the first salvo was fired from the US government. President Trump signed Executive Order 13873 [an obscure name given its importance]. This order tasked the Department of Commerce, working with other government agencies and departments, to address ICTS threats from “foreign adversary” countries. They had to (1) identify ICTS risks to national security and (2) define which countries were to be deemed “foreign adversaries” of the United States. They quietly began working quietly with these orders in hand. This included working with law enforcement and intelligence agencies to collect information and conduct investigations.

In 2024, four countries were identified as foreign adversaries: Russia, Iran, North Korea and China. This list was published just in time for President Biden to sign the “Protecting Americans from Foreign Adversary Controlled Applications Act” into law. Russia, Iran and North Korea don’t exactly have much by ways of ICTS applications in the United States. But China does – and TikTok is top of this list. The law specifically named TikTok and issued an ultimatum to its parent company ByteDance: divest TikTok USA as a stand-alone business to new US based owners or be banned in the United States. They were given 270 days (until Jan 19, 2025) to comply.

TikTok (ByteDance) tried to negotiate - it didn’t go well

Its hard to know what was going on inside TikTok’s corporate offices or the ByteDance headquarters in Beijing in response to the “divest or ban” law. But based on their proposals addressing US Government concerns, they seem to have had no idea how bad their position was. Throughout 2021 and 2022, they made several proposals to try and thwart the “divest or ban” threat. Suffice to say, their 3 proposals (listed below) were comically insufficient.

1. Proposed “operational independence” for US operations: TikTok proposed to (and later did) establish a new US based legal entity. This US entity would be staffed locally and be “operationally independent” from the ByteDance teams in China. But the recommendation engine software would continue to be designed, maintained and updated in China. But how can the US employees be operationally independent, while still totally dependent on software teams in China? American officials were unimpressed.

2. Data access rights from China based teams would be restricted: TikTok proposed to segment TikTok’s data (including sensitive personal data) into 3 categories, with ByteDance’s access restricted to certain data types only. But TikTok users would be able to “opt-in” to giving access to Chinese teams. Also, TikTok’s Terms and Conditions could be updated to get around the restrictions (by getting user consent to certain data sharing). I don’t know if the American officials involved in this process were less impressed with the first or second proposals.

3. Oracle (“trusted third party”) would audit the source code for TikTok’s recommendation engine and have a “kill switch”. This time, American officials didn’t even have to object. Oracle did it for them (perhaps worried about potential liabilities if they went along with this). They said they were not confident they could do a sufficient audit of the source code. Further, the proposed “kill switch” was only supposed to be temporary if a serious issue had to be fixed. And who would do the fix?

None of these proposals were deemed serious and the US Government, understandably, declined. The “divest or ban” ultimatum returned. In retrospect, TikTok should have moved to divest at that point. Instead, they sued. – saying that this “divest or ban” law infringed on their First Amendment rights, and those of their users. In doing so, they may have made things much harder for other Chinese social media companies in the United States (e.g. WeChat and XiaoHongShu “Little Red Book”).

TikTok runs full speed into the First Amendment - and it hurts

In December 2024, the US Court of Appeals (DC Circuit) denied TikTok’s petitions against the law in every dimension. There were 2 main challenges filed:

1. TikTok: “The government has not proven that we are controlled by the Chinese government”

The judges make it clear this is a poor argument based on considerable legal precedence. When it comes to national security, it is enough for the US Government to have any “informed basis” for their concerns. Their concerns simply have to be based on facts, not purely on hearsay. Whether the facts prove anything is not relevant. The courts defer to the Executive and Legislative Branches to determine national security concerns.

“[The Court] declines to second-guess the Executive’s judgement regarding a national security threat posed by the PRC” - US Court of Appeals (DC Circuit), Dec. 2024

2. TikTok: “The law singles us out explicitly, and is because US Government objects to our content”

TikTok alleged that the US government is targeting them explicitly because of their content. But the judge found this is clearly not the case. First, the law applies to any ICTS company controlled by a “Foreign Adversary” as designated by the Department of Commerce. TikTok is named only because it was identified as fit the criteria at the time the law was passed. In addition, the content on TikTok’s platform is not the target of the “divest or ban” law. Rather it is Chinese government control over that content. If TikTok divests to US owners (thereby ending Chinese government control), then they can remain operating in the United States (content unchanged). In short, the law is “content neutral” and does not single out a single platform.

“Specifically, the Government invokes the risk that the PRC might shape the content that American users receive, interfere with our political discourse, and promote content based upon its alignment with the PRC’s interests” - US Court of Appeals (DC Circuit), Dec. 2024

“Consequently, the Government does not suppress content or require a certain mix of content. Indeed, content on the platform could in principle remain unchanged after divestiture, and people in the United States would remain free to read and share as much PRC propaganda (or any other content) as they desire on TikTok or any other platform of their choosing. What the Act targets is the PRC’s ability to manipulate that content covertly. Understood in that way, the Government’s justification is wholly consonant with the First Amendment.” - US Court of Appeals (DC Circuit), Dec. 2024

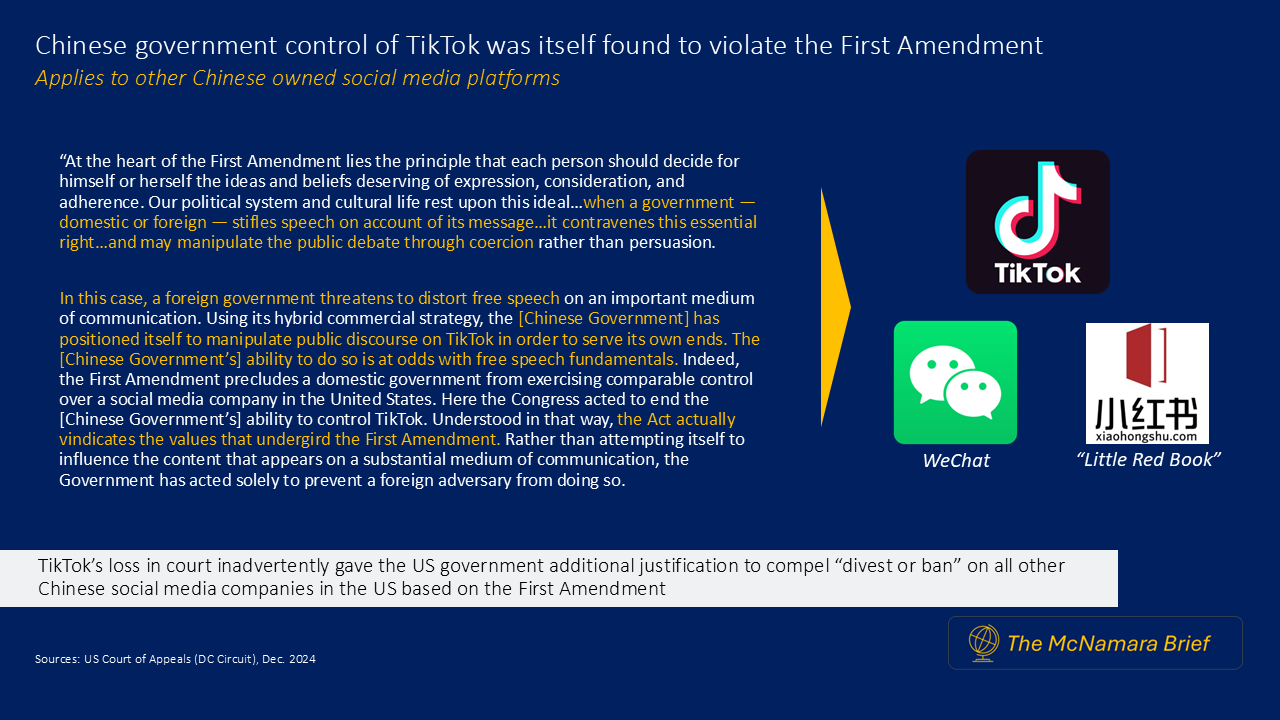

But this is where the ruling gets very interesting and has big ramifications for other Chinese owned social media platforms in the United States (e.g. WeChat, XiaoHongShu / “Little Red Book”). The judges cite extensive legal precedence to point out that if any government – foreign or domestic – had control over content on large social media platform, that this in of itself violates the First Amendment.

“At the heart of the First Amendment lies the principle that each person should decide for himself or herself the ideas and beliefs deserving of expression, consideration, and adherence. Our political system and cultural life rest upon this ideal…when a government — domestic or foreign — stifles speech on account of its message…it contravenes this essential right…and may manipulate the public debate through coercion rather than persuasion.

In this case, a foreign government threatens to distort free speech on an important medium of communication. Using its hybrid commercial strategy, the [Chinese Government] has positioned itself to manipulate public discourse on TikTok in order to serve its own ends. The [Chinese Government’s] ability to do so is at odds with free speech fundamentals. Indeed, the First Amendment precludes a domestic government from exercising comparable control over a social media company in the United States. Here the Congress acted to end the [Chinese Government’s] ability to control TikTok. Understood in that way, the Act actually vindicates the values that undergird the First Amendment. Rather than attempting itself to influence the content that appears on a substantial medium of communication, the Government has acted solely to prevent a foreign adversary from doing so” - US Court of Appeals (DC Circuit), Dec. 2024

The ramifications of this are potentially enormous. It means that TikTok, as it exists today, is in violation of the First Amendment due to its corporate structure (which likely applies to all Chinese social media companies operating in the US). China’s own laws giving effective control over content to the Chinese Government compel the “divest or ban” result.

At time of writing, the Supreme Court is hearing arguments in this case. No delay has been given for the TikTok ban, which should start in 4 days. Technically, President Trump (once inaugurated in 5 days) can give a 90-day extension to give time for TikTok to divest – but that’s basically it.

Given how much prior precedence was cited in coming to the current court ruling, it is hard to see the Supreme Court overturning any of it. Forced divestments of incredible Chinese businesses in the United States could make for interesting investment opportunities.

Is there money to be made here?

TikTok challenged the “divest or ban” law in court. In doing so, they likely did not expect to become the target of a First Amendment ruling. In some ways, this places added urgency to their divestiture. It has also started the clock (“Tik-Tok” if you’ll pardon the pun) on potential divestitures of other social media platforms.

These businesses are extremely valuable. In 2023, TikTok’s revenues were $16 billion in the United States (this number fell to $7.7 billion in 2024, but this was likely influenced by their legal problems). Meta, Snap and Pinterest trade at Price/Sales multiples of 6.6, 3.5 and 5.3 respectively. Taking the average of these three, a Price/Sales of 5.1 times $16 billion would value TikTok at $82 billion. Precise figures are not available for WeChat or XiaoHongShu, but they too would be very large divestitures. It is conceivable that these companies could soon come to public markets in the US. If this is the case, there could be a lot of money to be made. Prudent investors should monitor this space closely in the coming months and years.