The Hong Kong Dollar Peg: Is Stability a Mirage?

Following my first article on whether a looming currency crisis is coming for Hong Kong, Nikkei Asia reports confidence is eroding in the HKD to USD peg

A few weeks ago, I wrote about the Hong Kong Dollar (HKD) Peg and whether a currency crisis would again come to Hong Kong. The premise was that in 22 years, the “one country, two systems” agreement will formally expire, and the Hong Kong Dollar will disappear and be replaced with the Chinese RMB. It posed an important question: what incentive do Hong Kong residents have to keep their savings in Hong Kong Dollars today? They know they’ll eventually be forced to adopt the Chinese RMB – a significant devaluation, and they can access USD at a fixed exchange rate today. Would it not be better to convert to USD and hold those dollars outside of Hong Kong – out of government reach in case of any “sudden moves” from the local monetary authorities?

Recent reporting from Nikkei Asia has put Hong Kong Dollar peg squarely in the headlines – and potentially in question. While the peg's defenders cite substantial reserves and institutional resilience, the concerns raised about its long-term viability are getting much harder to ignore.

The McNamara Brief is a reader-supported publication. To receive new posts and support my work, please subscribe.

A Shield or a Shackle?

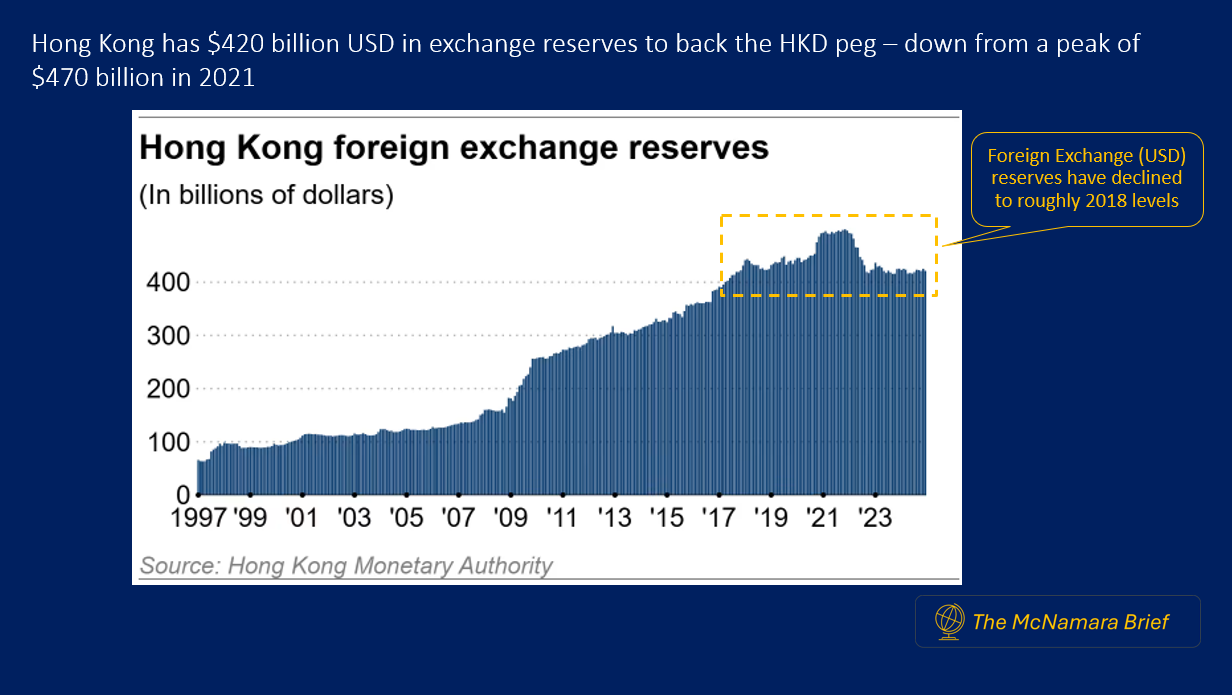

The Hong Kong Monetary Authority (HKMA) asserts that the peg remains essential for stability, and with $420 billion in foreign reserves, it seems well-equipped to defend it. Although reserves have declined from their peak in 2021, they claim there is no immediate cause for panic.

Yet, as the Nikkei Asia reports, this drop has raised questions about how much longer Hong Kong can rely on these buffers to sustain its currency linkage. This has become especially true as Hong Kong authorities have begun publicly discussing the sensibility of linking to the USD versus the Chinese RMB. Their premise: Hong Kong’s economy is more closely tied to China and the recent divergence in USD and RMB currencies has hurt Hong Kong’s economic prospects. For example, they cite higher borrowing costs in Hong Kong versus mainland China and dampening retail activity in Hong Kong as residents travel across the border to shop in China instead.

The pressure is building

Two scenarios are quietly adding pressure (1) potential US sanctions on China could upend the Hong Kong monetary system; (2) a gradual integration and usage of the Chinese RMB in Hong Kong could erode the HKD.

Sanctions are a possibility, but the issue triggering those sanctions would have to be quite severe for the US to go after a major conduit for USD funding in China.

The second scenario is likely to happen eventually in preparation for discontinuing the HKD [See my previous article on the HKD peg]. But it is unlikely to happen “naturally”. Right now, Hong Kong residents have no incentive to use the Chinese RMB. In fact, its the opposite – they get more for their money when they shop in China. Improved transit links mean residents can be in Shenzhen in under 30 minutes where their HKD goes much further than the local currency. For those that can get paid in HKD, but incur living expenses in RMB, they are feeling a “wealth effect” of their relatively strong currency. I suspect this wealth effect is quite popular. The Chinese RMB will eventually become more prominent in Hong Kong – but by government mandate, not market sentiment.

But do residents even have to know which scenario they face or when it could come? The incentive to convert to USD and transfer it out of Hong Kong is increasing rapidly. In fact, Nikkei Asia interviewed a Hong Kong based portfolio manager doing precisely that.

A Hong Kong-based portfolio manager at a China state-owned bank said he has been converting local currency into U.S. dollars, and putting those in several banks including a U.S. one. The manager, who declined to be named, cited concerns over accessing dollars saved in a local bank if it is cut off from SWIFT, the dominant global payments system that is partly overseen by the Fed.

Hong Kong authorities should dread this. I suspect finance professionals and portfolio managers are already “hedging their bets” and that the race for the exits has slowly begun. Whether the trigger is concern over potential sanctions, HKMA policy shift or the eventual end of “one country, two systems” is irrelevant for those holding their wealth in HKD. I return to the question of my first article: Is a HKD currency crisis inevitable? The HKD may seem stable for now, but it seems confidence is eroding.