Capital One's $35 Billion Power Play

Acquiring Discover to Challenge the Payments Duopoly...or a High-Stakes Wager with Uncertain Payoff?

Picture this: A data-driven lender absorbs a network operator, creating a $660 billion entity poised to disrupt Visa and Mastercard’s dominance. But with fresh regulatory battles and escalating integration expenses, was this 2024 announcement a strategic masterstroke or an overvalued risk? Explore the mechanics, metrics, and implications for banking in 2026.

What if a single transaction could dismantle the entrenched duopoly in U.S. payments processing, generate billions in synergies, and elevate a regional player to national prominence—while navigating intense antitrust review and investor skepticism? That was the core proposition of Capital One’s $35.3 billion all-stock acquisition of Discover Financial Services, unveiled in February 2024 and consummated on May 18, 2025, following a protracted regulatory process. As of March 2026, with one year of integrated operations, the results are unfolding: robust revenue growth and stabilizing credit quality, tempered by persistent ROE declines and integration costs exceeding initial estimates.

Building on my prior analysis of Cisco’s $28 billion acquisition of Splunk, where understated projections potentially left significant value untapped, this examination dissects the Capital One-Discover transaction for deal professionals and enthusiasts. We will detail the strategic rationale, trace the negotiation chronology, analyze the valuation framework in depth, evaluate its assumptions, review regulatory challenges, compare to analogous deals, assess post-merger outcomes, and extract key insights.

Strategic Rationale: Capital One’s Push for Scale and Independence in a Competitive Landscape

In consumer finance, where data analytics and network control drive margins, acquisitions are essential for maintaining competitiveness. Capital One, established in 1994 as a credit analytics specialist, had amassed $482 billion in assets through targeted lending products like the Venture rewards card and retail partnerships. However, by 2023, it faced pressures including elevated delinquencies in subprime segments, competition from FinTechs such as Affirm, and substantial fees paid to Visa and Mastercard for transaction processing.

Discover, with $143 billion in assets, offered a complementary profile: a focus on prime borrowers, a proprietary payment network processing 4% of U.S. card volume and extending to over 200 countries through Diners Club and PULSE, and a strong debit business. Despite these strengths, Discover contended with operational issues, including a 2023 card misclassification incident resulting in a $365 million charge and FDIC enforcement actions, alongside a CEO transition that pressured its stock.

The deal’s value proposition centered on vertical integration. Capital One anticipated $2.7 billion in pre-tax synergies by 2027, comprising $1.5 billion in cost reductions from eliminating overlaps in technology, branches, and operations, and $1.2 billion in revenue enhancements from internal debit routing, which could reduce interchange fees by 20-30%. Beyond efficiencies, the merger enabled cross-selling of premium products to Discover’s 100 million customers, advanced AI applications in lending, and broadened merchant networks to 70 million acceptance points. Following closure, Capital One shifted toward higher-end segments, reducing subprime exposure to emulate American Express’s model while enhancing fraud prevention through aggregated data.

“Critics are wary of the size of the deal, but some analysts say it could create a stronger challenger to Visa and Mastercard.” - Bloomberg

Challenges were evident: Potential cultural mismatches between Capital One’s agile culture and Discover’s established systems risked employee attrition, with 1,100 Discover positions eliminated by March 2026. Technology migrations posed outage risks, and antitrust concerns over the combined 30% subprime market share necessitated a $265 billion community benefits commitment, which critics argued overstated new investments at under $5 billion according to organizations like the National Community Reinvestment Coalition. Nevertheless, the merger promised to chip away at Visa and Mastercard’s over 80% market control, potentially lowering merchant costs over time.

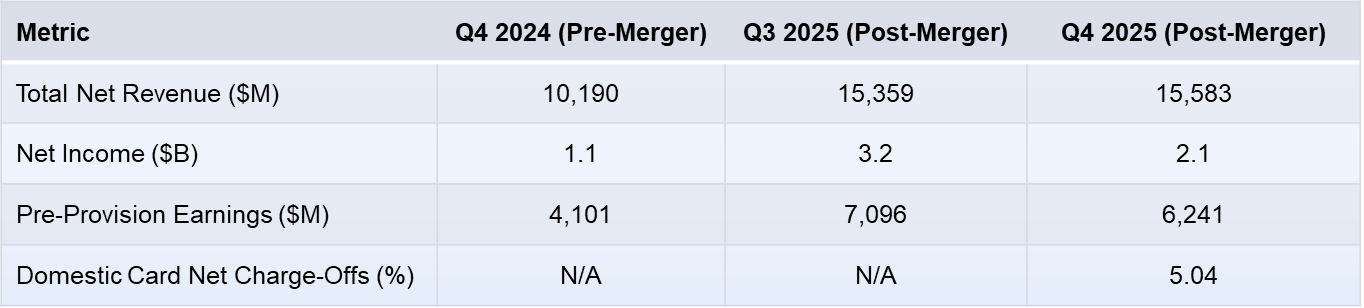

One year post-closure, performance indicators show progress amid headwinds. Third-quarter 2025 revenues increased 23% year-over-year to $15.4 billion, bolstered by Discover’s assets, with organic purchase volumes rising 6.5%. Credit trends improved, with domestic card net charge-offs at 5.04% and delinquencies at 3.93% in early 2026. However, integration expenses exceeded projections, contributing to a $4.3 billion net loss in Q2 2025 from acquisition-related accounting, including $510 million in quarterly intangible amortization. Return on equity fell to 9.63%, below the sector average of 9.78%, leading to analyst downgrades such as Seeking Alpha’s Strong Sell rating, which forecasts an 11.6% downside to a $160.90 fair value due to efficiency shortfalls.

Negotiation Chronology: Mapping the Path from Initial Outreach to Regulatory Approval

Large-scale mergers require meticulous orchestration, often spanning months of discussions, assessments, and adjustments. Similar to the Splunk-Cisco process (initial engagement in 2021 leading to closure in 2023), the Capital One-Discover timeline involved strategic pauses and escalations and complexities.

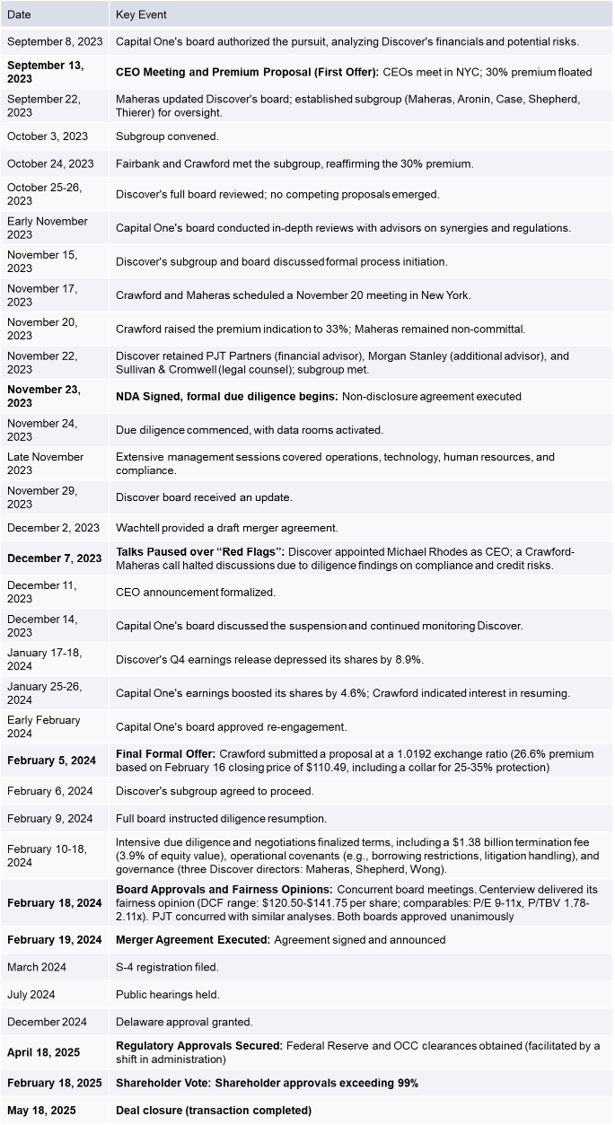

The groundwork predated 2023, with both companies periodically evaluating growth opportunities amid rising interest rates, fintech competition, and regulatory pressures. Discover maintained independence but entertained advisor contacts following its July 2023 misclassification issue, which incurred a $365 million liability and prompted an FDIC consent order.

The process accelerated in August 2023: Discover’s CEO resigned on August 14, causing a stock decline. Chairman Thomas Maheras received inquiries, including from Stephen Crawford, an advisor to Capital One CEO Richard Fairbank, around mid-August. This led to a September 13 meeting in New York, where Fairbank proposed a stock-for-stock transaction at a 30% premium. Capital One had engaged Centerview Partners and Wachtell, Lipton, Rosen & Katz by mid-August.

In December 2023, the merger discussions between Capital One and Discover hit a significant roadblock when Capital One’s due diligence uncovered critical red flags related to Discover’s compliance and credit risk management. Key issues included a long-standing card product misclassification dating back to 2007, where certain credit card accounts were incorrectly placed in higher merchant pricing tiers, resulting in ongoing merchant settlement discussions, regulatory scrutiny, and an SEC investigation. Discover had already recognized approximately $290 million in estimated penalties as of September 30, 2024, tied to a 2023 FDIC consent order mandating enhancements to consumer compliance, governance, and risk practices. Additionally, concerns arose over the adequacy of Discover’s compliance management system and credit risk framework, which Capital One deemed insufficient for alignment with its standards and regulatory expectations. These findings prompted Capital One’s management to inform Discover on December 7 that it would not proceed, citing the diligence status and external factors like Discover’s rising stock price, which would necessitate a higher exchange ratio.

The temporary halt, reviewed and affirmed by Capital One’s board on December 14, highlighted the potential for substantial remediation costs—estimated within the overall $2.8 billion in acquisition and integration expenses, including one-time fixes for Discover’s issues—and raised uncertainties around regulatory approvals, operational integration, and financial synergies. This pause delayed the process by several weeks, allowing time to assess whether the risks outweighed the benefits, but discussions resumed in January 2024 after market shifts and further evaluations, ultimately leading to the deal’s revival and completion.

Valuation Framework: A Detailed Examination of Projections, Dividend Discount Model, and Comparable Transactions

Valuations in this transaction were based on structured analyses by financial advisors Centerview Partners (for Capital One) and PJT Partners (for Discover). These relied on unaudited management projections, emphasizing conservatism amid economic uncertainty. The analyses incorporated standalone forecasts for both companies, adjusted for synergies, and excluded certain one-time items like Discover’s student loan portfolio disposition (implied NPV of ~$7.25 per share, excluded due to uncertainty). Below, we break down the key components into management projections, the dividend discount model (used as a proxy for DCF), and market comparables.

Management Projections: Building Blocks of Standalone and Synergized Forecasts

The unaudited prospective financial information formed the core inputs, derived from consensus estimates (e.g., from FactSet or street research) for near-term years (2024-2025) and extrapolated for longer horizons (up to 2030, varying by advisor). These projections included net income available to common shareholders (NIAT), earnings per share (EPS), return on average tangible common equity (ROATCE), tangible book value per share (P/TBV), risk-weighted assets (RWAs), total loans, and total capital returns (e.g., dividends and buybacks). Assumptions reflected steady growth amid economic headwinds, with Capital One targeting CET1 ratios of 13% and Discover 12% for capital adequacy. Synergies were layered on top: $2.7 billion pre-tax by 2027

For Capital One standalone (Centerview’s view, 2024-2030; extrapolated with ~1% NIAT growth in 2026 and ~3% thereafter; RWAs ~3.5% annual growth from 2026)

PJT’s Capital One standalone projections (2024-2028; NIAT growth 13% in 2025, 7% thereafter; loans/RWAs ~5% annual growth from 2025; capital returns at 68% payout ratio)

For Discover standalone (Centerview’s view, 2024-2030; NIAT growth ~8% in 2026, 5% in 2027, 11% in 2028-2029, 4% in 2030; RWAs ~3% in 2026, 5% thereafter; 2024 includes student loan sale impact)

PJT’s Discover standalone projections (2024-2028; NIAT growth ~10% annual average; loans/RWAs ~7-8% growth)

Dividend Discount Model: Discounting Future Cash Flows to Present Value

The primary valuation method was a dividend discount model (DDM), serving as a proxy for discounted cash flow (DCF) tailored to the banking sector. DDM was preferred over traditional DCF because banks’ cash flows are heavily constrained by regulatory capital requirements (e.g., Basel III and CET1 ratios), making free cash flow unpredictable and less relevant—leverage and capital structure are integral to operations, not separable as in non-financial firms. Instead, DDM focuses on distributable dividends (excess cash after maintaining capital buffers), providing a more accurate reflection of shareholder value in a regulated environment where dividends are stable and tied to risk management. This approach aligns with financial institutions’ unique dynamics, where working capital and capex have minimal impact, and earnings are often directed toward reserves rather than unrestricted FCF.

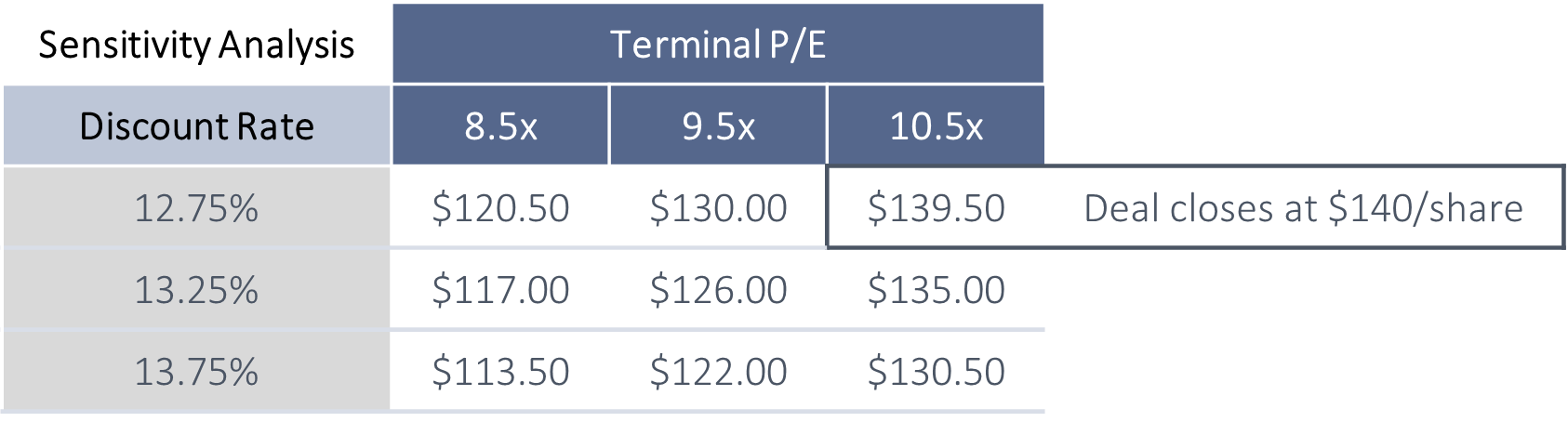

Centerview and PJT applied sensitivities to growth, discounts, and terminals, yielding implied per-share ranges for Discover. Centerview’s DDM (2024-2030 forecasts; discount rates 12.75-13.75% via CAPM: 4% risk-free, 1.4-1.5 beta, 5-6% equity risk premium; terminal P/E 8.5-10.5x on 2030 NIAT; perpetual growth implied ~2-4% in sensitivities): Implied Discover value $120.50-$141.75 per share (standalone), adjusting for synergies to support the exchange ratio (0.88-1.23x ex-synergies, 1.06-1.75x incl.).

PJT’s DDM (2024-2028 forecasts; discount rates 11-13%; terminal P/E 8.5-10.5x on 2028 NIAT): Implied Discover value $117.46-$145 per share.

Market Comparables: Benchmarking Against Peers and Precedents

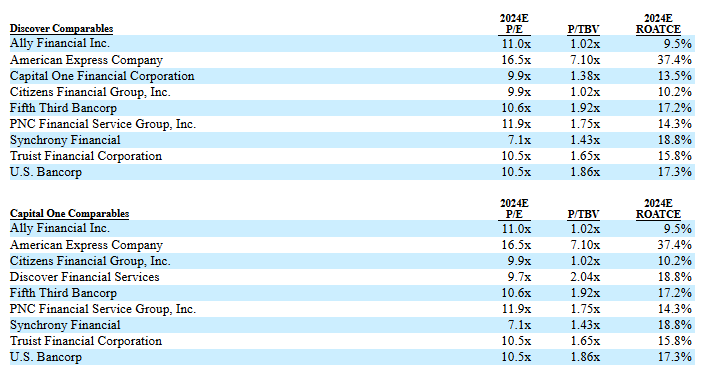

Comparables analyses supplemented DDM, using selected public companies for multiples and precedent transactions for premiums. Peers were chosen for similarity in consumer finance/banking (e.g., focus on cards, lending).

These supported the deal’s premium as aligned with market norms, though critics noted limited fintech inclusion.Centerview’s comparable companies: P/E (9-11x 2024E EPS) and P/TBV (1.78-2.11x via ROATCE regression) for peers like American Express, Ally Financial, Synchrony Financial. Implied Discover ranges: $107.75-$130 (P/E), $103.25-$121 (P/TBV).

PJT’s similar: P/E 9-11x, P/TBV 1.78-2.11x, yielding overlapping ranges.

Premiums paid: 10-35% applied to Discover’s unaffected $110.49 price (February 16, 2024 close), implying $121.50-$149.25 per share.

Precedent transactions (selected banking deals) informed the range but were not detailed with specific multiples.

Reviewing the P/E comparables we see overlap with the sensitivity analysis and a rough triangulation approach on the final deal value at a roughly 10.5x P/E. This represented a 27% premium to Discover’s market value at the time of the deal.

Scrutinizing the Valuation: Assessing Assumptions and Potential Enhancements

The 27% premium appeared reasonable given Discover’s challenges, but parallels Splunk-Cisco’s conservative approach, where growth projections may have understated potential. NIAT forecasts (3-11% for Discover) overlooked opportunities in network globalization or AI enhancements. Discount rates (11-13.75%) were elevated; reducing to 10-12% might increase per-share value by $10-20.

Comparables were appropriate but limited; incorporating fintech benchmarks like SoFi (12-15x P/E) could justify higher multiples. The premiums range was expansive; a 20-30% banking median aligns with the deal’s 27%, yet deeper precedent transactions (e.g., Synchrony-Ally alignments) were underemphasized. Without alternative scenarios (e.g., 5-7% perpetual growth if synergies surpass $2.7 billion), Discover may have conceded $5-10 billion. Analyst views diverge: BTIG’s post-closure Buy rating cites $21.39 EPS potential, while others highlight ROE shortfalls, estimating fair value at $161.

Navigating Regulatory Hurdles: The Beltway Battles That Shaped the Outcome

Regulatory approval in banking mergers extends beyond financials to public policy. Antitrust concerns over subprime concentration attracted Department of Justice criticism, with groups like the American Economic Liberties Project deeming it anticompetitive and predicting fee hikes. Capital One rebutted by emphasizing network competition, though detractors questioned the efficacy of claimed efficiencies.

The process: Applications filed March 2024; July public hearings; extensions under Biden-era stringency. A post-election administrative change in April 2025 expedited Federal Reserve and OCC approvals, alongside Delaware clearance in December 2024. The $265 billion benefits package (focused on low- to moderate-income lending and branch expansions) was promoted as transformative but critiqued for minimal incremental value.

“Regulators have been tough on big financial mergers, though there are nuances in Capital One’s $35.3 billion takeover bid for Discover.” - New York Times

Benchmarking Against Peers: Contextualizing the Deal in Banking’s Consolidation Wave

To evaluate Capital One-Discover, consider it alongside 2025’s heightened M&A activity (over 150 announcements, with October’s $21.4 billion marking the peak since 2019). Comparisons include Fifth Third-Comerica, Huntington-Cadence, PNC-BBVA (2021 benchmark), and cross-sector to Splunk-Cisco.

Fifth Third’s $10.9 billion all-stock Comerica deal (announced October 6, 2025; expected Q1 2026 close) aimed for regional dominance, yielding a $288 billion entity with leading positions in the Midwest and Texas. The 1.8663 exchange ratio provided a 20% premium to Comerica’s 10-day VWAP ($82.88 implied). Synergies: $850 million gross pre-tax (35% of Comerica’s 2026 expenses), with revenue opportunities in payments and wealth. Timeline: Comerica explored options in summer 2025 amid liquidity issues; CEO contact September 18; Dallas meeting September 19; nonbinding indication September 23; finalization through September 30; execution October 5. Advisors mirrored Capital One’s (Goldman Sachs, J.P. Morgan). Valuations: Conservative DCF/comps supported fairness, with risks in integration and enhanced regulatory category. Unlike Capital One’s network focus, this emphasized footprint expansion, with milder antitrust but comparable community commitments.

Huntington’s $7.4 billion Cadence acquisition (mid-2025 announcement) created a $276 billion top-10 bank via Sunbelt growth and deposit diversification. Valuation: 1.5x tangible book value premium; synergies $800 million (30% cost reductions). Shorter timeline (6 months to close) leveraged regulatory easing. Early 2026 data indicates 15% EPS accretion but initial ROE pressure—echoing Capital One’s trajectory with less subprime exposure.

PNC’s $11.6 billion cash purchase of BBVA USA (announced November 2020; closed June 2021) offers historical perspective: 1.34x TBV and 19.7x 2019 earnings, with $900 million synergies (35% of BBVA expenses) forming a $560 billion national player. Integration overruns ($980 million expenses) delayed benefits, akin to Capital One’s cost escalations. Outcomes: 21% 2022 EPS lift, though the $88 billion benefits plan faced scrutiny—similar to Capital One’s. PNC achieved >19% IRR, illustrating long-term rewards despite early hurdles.

Post-Merger Assessment: Progress, Pain Points, and Forward Outlook

Retrospective analysis highlights resilience: Q3 2025 revenues rose 23%, with synergies advancing (e.g., debit routing implemented early 2026). Yet, Q2’s $4.3 billion loss, cost overruns, and subprime portfolio adjustments underscore challenges. Capital returns via $16 billion buybacks and dividend increases supported shares, but ROE declines indicate ongoing inefficiencies. Credit trends reflect normalization, with charge-offs steady and reserves easing.

“The Discover acquisition drove double-digit growth, but organic card spending and loans also expanded.” - PYMNTS

“[integration costs] will surpass the original $2.8 billion estimate.” - Capital One CEO Richard Fairbank stated during the Q2 2025 earnings call

The company added that it’s still on track for $2.7 billion in total net synergies, due to cost savings and revenue synergies from the combination. But it seems this is taking far longer to achieve than originally anticipated.

Key Insights and Implications: Synthesizing Lessons for Future Transactions

The Capital One-Discover merger exemplifies M&A’s capacity to transform sectors: a calculated integration of networks and data that navigated negotiations, valuations, and regulations to yield a payments contender. It demonstrates how deals emerge (opportunistic timing during vulnerabilities), valuations are constructed (through layered projections and sensitivities), and improvements can be made (by incorporating upside cases to maximize outcomes).

For dealmakers, the takeaways are pragmatic: Align pursuits with market lows for favorable premiums; integrate diligence pauses as risk mitigators; broaden comparables to include emerging peers; and prepare for regulatory variability, where shifts can compress timelines. In banking’s ongoing consolidation, this transaction signals opportunities in tech-enabled scale but warns of execution risks. Conservative assumptions can protect against downside, but can deprive shareholders of real value.