Fannie Mae ($FNMA) and Freddie Mac ($FMCC): A simple and lucrative business model

Two of the largest financial institutions in the world could soon return to public markets. For investors with an appetite for risk, the returns could be enormous.

This is a follow-up on a previous report covering the history of Fannie Mae and Freddie Mac and how they arrived in their current predicament being under government conservatorship. In this report, I focus on their business models, financial performance and develop an investment thesis and price target. The detailed content of this article is mostly behind a paywall. Please subscribe to unlock.

A Simple, Lucrative Business Model

The business models of Fannie Mae and Freddie Mac are simple. They each operate two business categories: (1) Securitization and Guarantee Business and (2) Retained Portfolio business. The Securitization and Guarantee Business is by far the most important, as the Retained Portfolios have been effectively wound down and will be a negligible part of their earnings going forward.

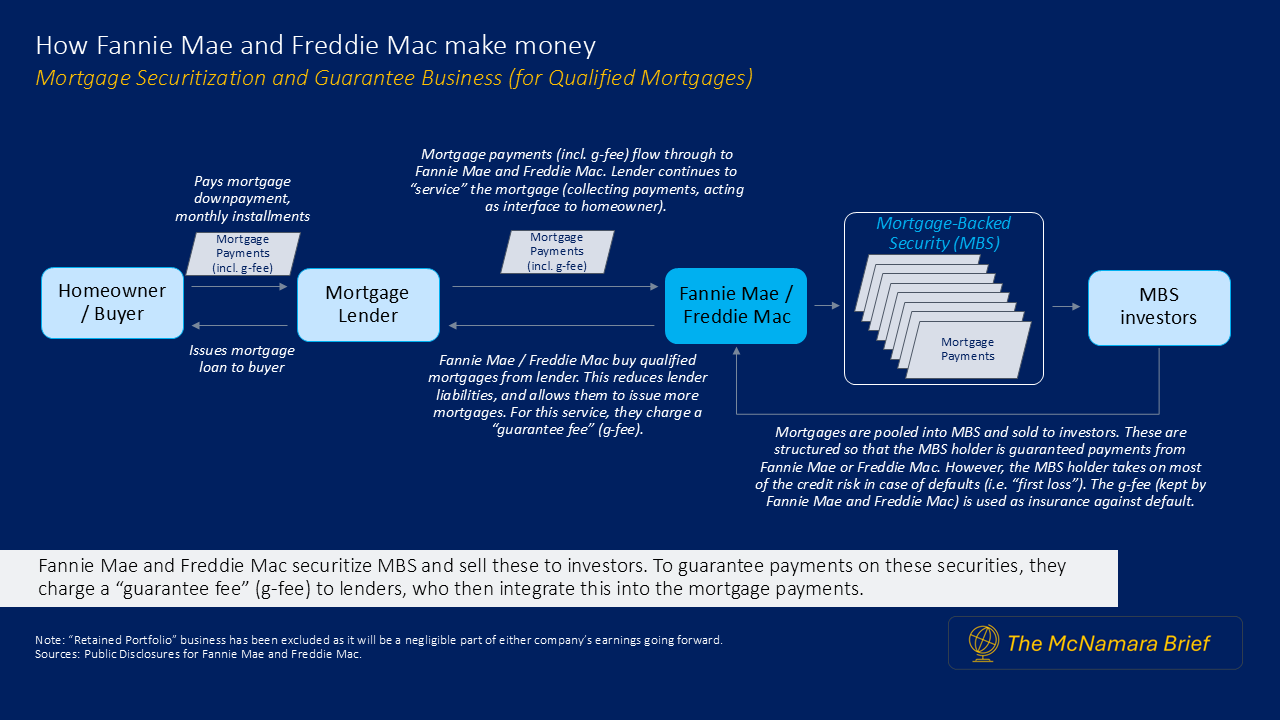

Securitization and Guarantee Business

The companies acquire “qualified” mortgages from lenders, bundle them into pools of Mortgage-Backed Securities (MBS), and sell these securities to investors. They guarantee the timely payment of principal and interest on these securities by charging a “guarantee fee” (g-fee) to lenders for this service. Lenders pass on the fee to the homeowner. This fee has ranged from 50 to 60 basis points in recent years. It is embedded in the mortgage rate itself – making it largely unnoticed by homeowners.

The companies take on two main risks associate with this business line: Credit Risk and Pre-Payment Risk. Credit risk is the risk of a borrower defaulting on their mortgage. Pre-Payment Risk is the risk that borrowers refinance their mortgage (or otherwise pay off) their mortgage earlier than expected, thereby affecting the g-fee income stream.

To mitigate against Credit Risk, there are strict underwriting standards for mortgage eligibility. The g-fees are priced based on risk (i.e. they charge more for riskier mortgages, or to borrowers with lower credit scores). They also use g-fee income to build capital reserves to cover potential losses. In recent years, they have introduced a Credit Risk Transfer system by selling portions of risk to investors. To mitigate against Pre-Payment Risk, the companies structure MBS pools with callable or non-callable options that can manage pre-payment speeds. There are also complex hedging strategies to offset the financial impacts of pre-payments.

The g-fees charged are meant to provide capital to cover any potential losses arising from Credit or Pre-Payment Risk. Importantly, housing is one of the areas where extensive long-term data sets are available. Forecasting risk becomes relatively straightforward. Capital reserves are built to withstand shocks to the housing finance system that occur very infrequently [Note: Dodd-Frank Stress Tests are conducted annually to mimic another Financial Crisis and determine capital sufficiency. In recent years, both companies have passed easily]. The g-fee business has proved extremely resilient over time.

Retained Portfolio Business (“pre-2008”)

Both companies also maintain a “retained portfolio” where they acquire mortgages from lenders, but retain them instead of selling MBS to investors. Naturally, this comes with Interest Rate Risk as well as Credit Risk and Liquidity Risk. However, this business consists of mortgage pools on their books from before the 2008 Great Financial Crisis. Regulations introduced after 2008 prevent the companies from re-entering this space. The legacy pools of mortgages have largely run off their books by the time of this publication. Going forward, their contribution to either Fannie Mae or Freddie Mac’s income streams will be effectively negligible.

The business model has scaled with the size of the US housing and MBS markets, and has proven to be highly lucrative over time. The Retained Portfolio was the source of trouble for both companies during the Great Financial Crisis, not the Securitization and Guarantee Business. Going forward, they will only be in the Securitization and Guarantee Business.

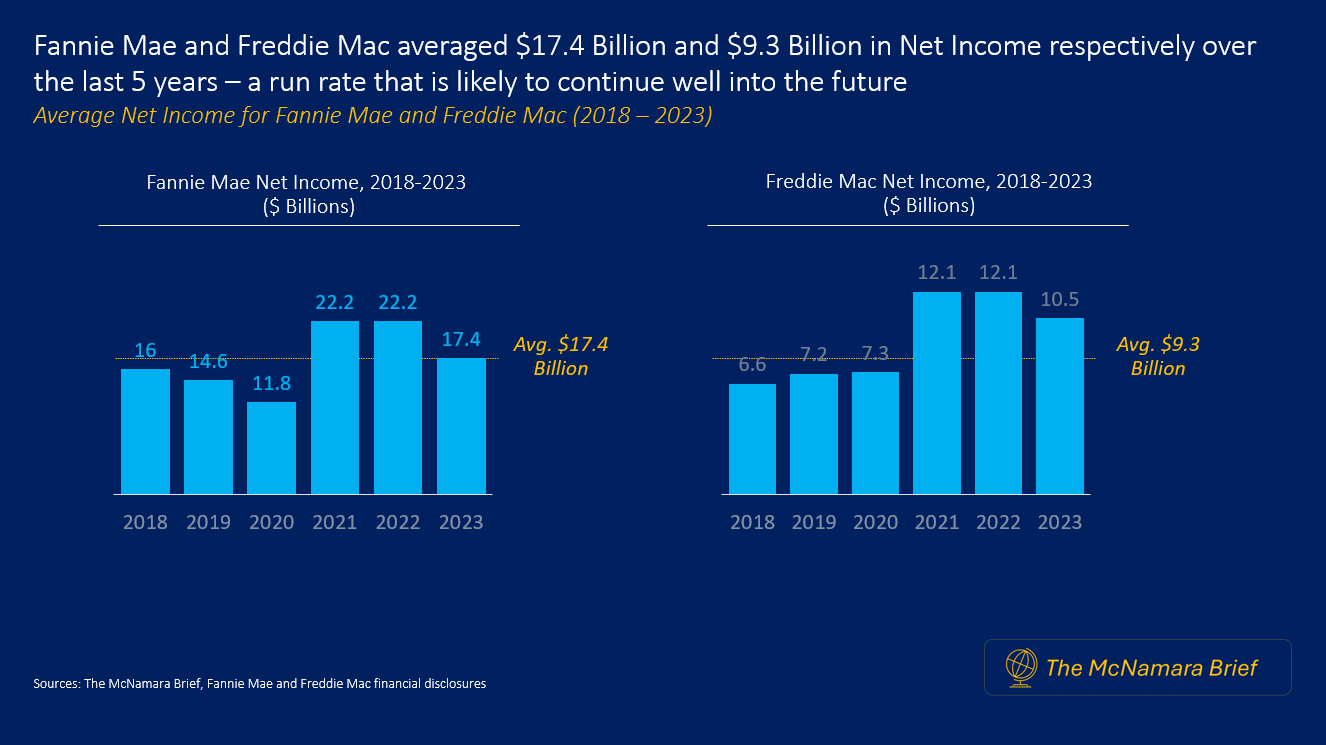

Net income has averaged $17.4 billion and $9.3 billion for the last 5-years for Fannie Mae and Freddie Mac respectively. These enormous returns are very stable and could command a high valuation if/when their conservatorships end.

An investment thesis emerges

At time of writing, a new Trump administration is preparing to take office. There is considerable speculation about this new administration moving to end the conservatorships. There is also considerable uncertainty that needs to be recognized. The biggest question is what Treasury will do with their existing SPS obligation.